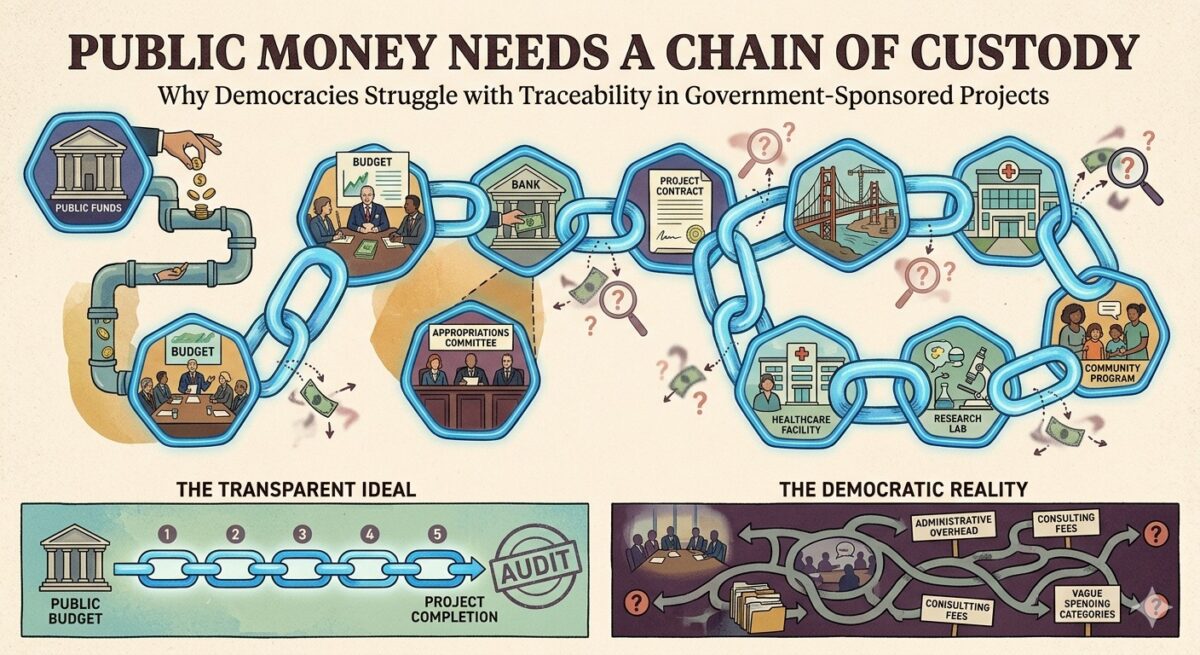

When a private company loses track of project money, auditors call it a control failure. When a government loses traceability of public money, citizens often call it corruption. But the truth is more complex.

A lack of traceability does not always mean money was stolen. It may mean the money moved through too many accounts, too many agencies, too many budget heads, too many contractors, or too many undocumented decisions. But that is precisely why it is dangerous. Once the audit trail breaks, nobody can confidently say whether money was used for its intended purpose.

This problem is not limited to poor countries or authoritarian regimes. Democracies also face it. In fact, democracies may be especially vulnerable when elected governments borrow, announce, allocate, reallocate, and spend public funds faster than accounting systems, audit institutions, and citizens can follow.

The central issue is simple:

A democracy may approve a budget, borrow money, and report expenditure — yet still fail to prove that money reached the intended project, asset, contractor, beneficiary, or outcome.

That gap between money spent and money traceably used is where public-finance risk lives.

Traceability is not the same as expenditure

Governments often defend themselves by saying, “The funds were received” or “The funds were utilized.” But both statements can be incomplete.

A proper traceability chain should answer:

- Where did the money come from?

- Which treasury or project account received it?

- Under which budget head or project code was it booked?

- Which department or agency received it?

- Which contract, invoice, or beneficiary payment used it?

- Which physical asset, service, or outcome was created?

- Who verified completion, quality, quantity, and value for money?

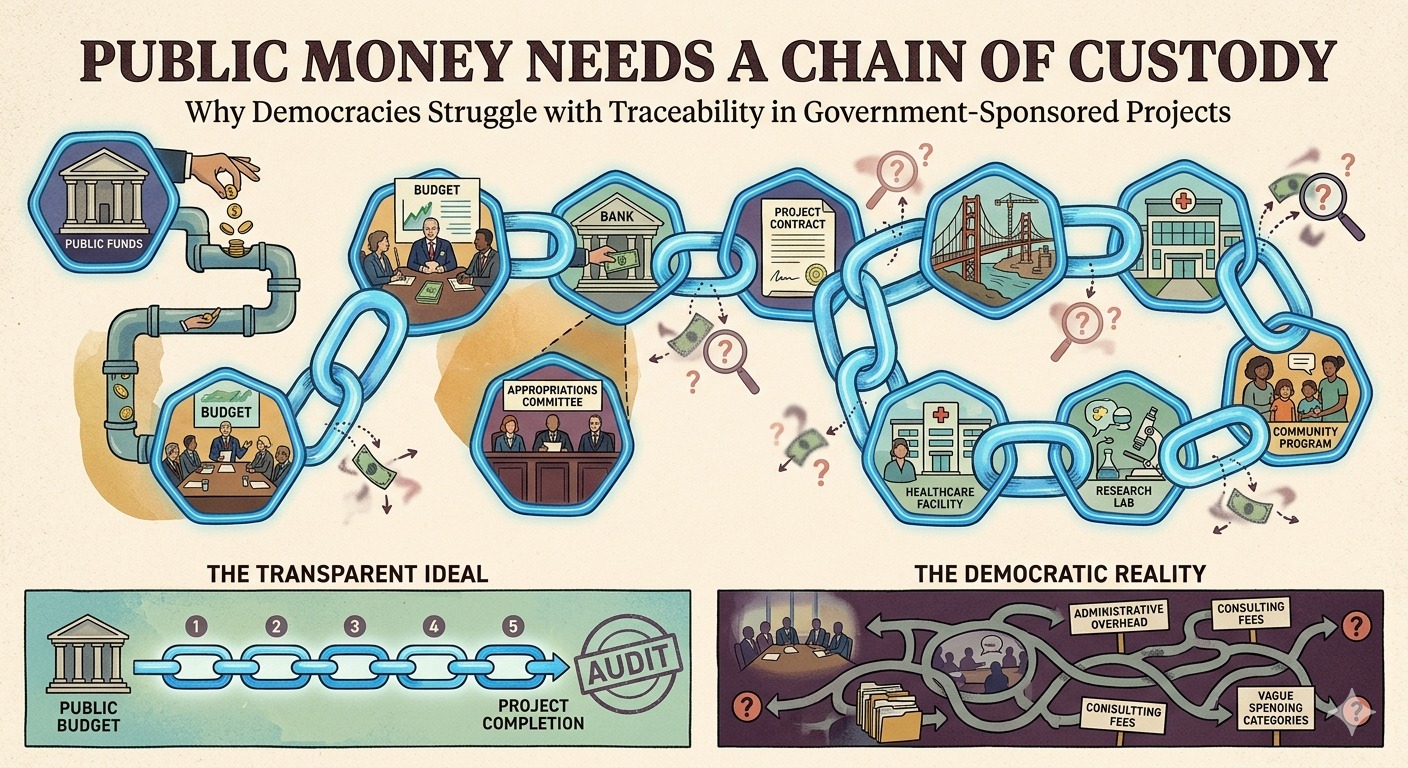

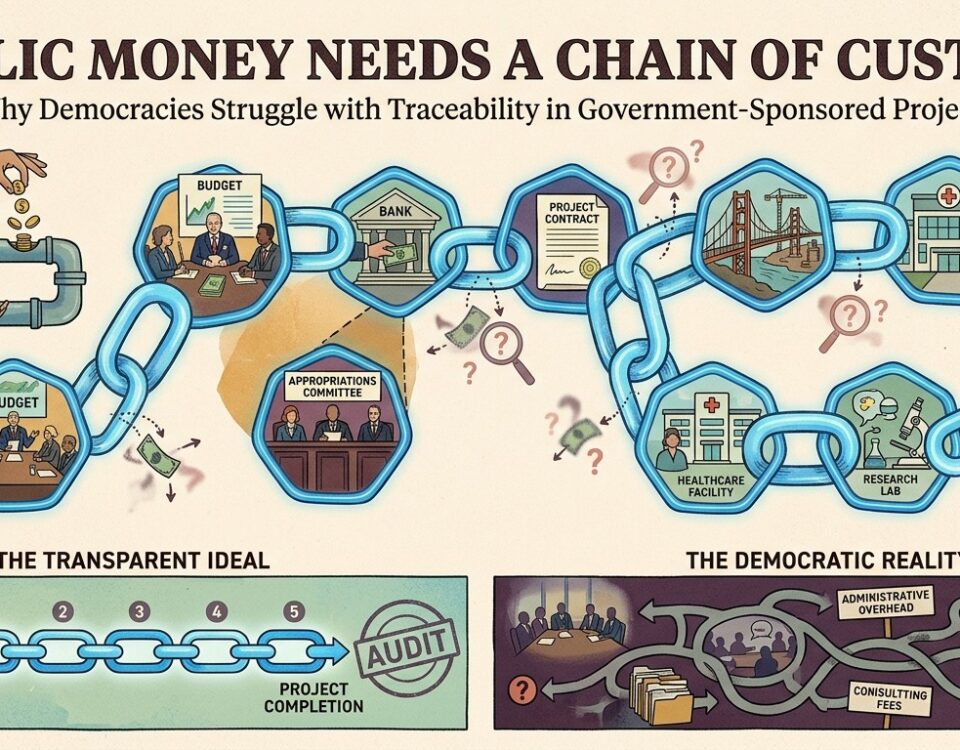

In engineering terms, public money needs a chain of custody.

If steel is used in a bridge, a good quality system traces the heat number, mill certificate, test report, purchase order, delivery challan, inspection report, and final location of installation. Public money deserves the same discipline.

Without that chain, a government may still be able to say, “Funds were spent,” but it cannot convincingly say, “Funds created the promised public value.”

The Kenya Eurobond case: money entered the Exchequer, but project traceability failed

The Kenya Eurobond case is a sharp example. The Auditor-General’s special audit confirmed that Eurobond proceeds entered the National Exchequer Accounts. But it also concluded that the utilization of those proceeds could not be traced to specific development projects. The National Treasury explained that the funds were fungible, and the audit further noted that some expenditure occurred outside the Government Integrated Financial Management Information System. The Auditor-General therefore recommended that future sovereign bond issuances be earmarked and identifiable to specific development projects.

This distinction matters. It is possible for money to enter the government treasury and still lose project-level traceability. In the Kenya case, the issue was not merely whether money arrived. The deeper question was whether citizens could see which roads, power projects, public assets, or development works were financed by that borrowing.

This is the difference between treasury-level confirmation and asset-level accountability.

The Mises article that triggered this discussion uses Schumpeter and Rothbard to frame the scandal politically: Schumpeter viewed democracy as a competition among political elites for power, while Rothbard’s “cui bono?” asks who benefits from state action. The article’s claim is that public borrowing, when poorly constrained, can become a tool through which political winners control large resources while taxpayers inherit the debt. (Mises Institute)

Whether one agrees with the article’s ideological framing or not, the traceability problem is real: once borrowed money enters a large public-finance pool, the public must rely on strong accounting, audit, and project-management systems to know what happened next.

Why this happens in democracies

The problem is structural. Democratic governments operate through ministries, departments, state agencies, local bodies, public enterprises, special purpose vehicles, autonomous bodies, contractors, subcontractors, and beneficiaries. Money often moves through multiple layers before it becomes a road, bridge, hospital, classroom, transformer, software platform, or welfare payment.

At every layer, traceability can weaken.

A central government may release funds to a state. A state may release funds to a department. A department may release funds to a district or local body. The local body may engage a contractor. The contractor may subcontract. Payments may be split across advances, running bills, escalation claims, retention amounts, and final bills.

Unless every layer uses a common project ID, common digital trail, and common audit architecture, the financial record becomes fragmented.

This is why modern public-finance reforms emphasize systems such as Treasury Single Accounts and Integrated Financial Management Information Systems. A World Bank toolkit explains that a centralized Treasury Single Account is designed to capture revenue and expenditure transactions through a consolidated structure of bank accounts, while also noting that decentralized arrangements make it more difficult to capture transaction details. (World Bank)

But even a Treasury Single Account does not automatically solve project traceability. It improves cash control. It does not, by itself, prove that a specific loan, grant, or budget release produced a specific asset.

India’s utilisation certificate problem: expenditure without timely proof

India provides a familiar example through the issue of Utilisation Certificates, or UCs.

A UC is supposed to certify that a grant was used for the purpose for which it was given. In principle, this is a basic accountability document. In practice, pending UCs are a recurring public-finance problem.

In Maharashtra’s urban local bodies, CAG reported that as of June 2022, 760 utilisation certificates for grants amounting to ₹13,645.33 crore released up to March 2021 were pending from field offices. CAG also observed inadequate internal controls such as non-reconciliation of cashbooks with passbooks, improper or incomplete cashbooks, and non-maintenance of separate cashbooks for different schemes.

This is not automatically proof that the money was stolen. But it means the audit trail was weak. If a grant is released for a specific purpose, and the certificate proving its use is pending for years, then the system is asking citizens to trust expenditure without timely evidence.

From a risk-engineering perspective, this is a classic control failure. The money may have moved, but the documentation has not caught up with the money.

The United States: payment integrity failures in a high-capacity democracy

Developed democracies are not immune. The United States Government Accountability Office reported that in fiscal year 2025, federal agencies estimated about $186 billion in improper payments across 64 programs. GAO also stated that these estimates do not represent the full extent of government-wide improper payments, and that some payments are treated as improper when their propriety cannot be determined due to lacking or insufficient documentation. (GAO)

This is important. Improper payment does not always mean fraud. It can mean overpayment, underpayment, payment to an ineligible recipient, payment without sufficient documentation, or payment where correctness cannot be verified.

That last category is especially relevant to traceability. A payment that cannot be verified due to insufficient documentation may represent a governance failure even when no criminal intent is proven.

The lesson is uncomfortable but necessary: even sophisticated democracies can spend large sums without having perfect assurance over payment correctness.

The United Kingdom: when audit itself becomes delayed

The United Kingdom offers another example from the audit side. The National Audit Office disclaimed the UK Whole of Government Accounts for 2023–24 for the second successive year. The NAO said the cause was the lack of audited accounts from English local authorities, creating inadequate assurance over material amounts throughout the national accounts. Only 4% of English local authorities submitted adequate audited data for inclusion in the 2023–24 Whole of Government Accounts; 41% submitted no data, and 55% submitted unaudited data. (National Audit Office (NAO))

Again, this does not mean public money was stolen. It means the assurance system failed to provide reliable audited information on time.

A democracy depends not only on elections, but also on credible accounts. If local authorities cannot produce audited data, national accounts become less reliable. Public scrutiny weakens. Citizens cannot properly judge whether money was well managed.

The European Union: even advanced funding systems face final-recipient opacity

The European Court of Auditors recently examined the EU Recovery and Resilience Facility, a large post-COVID recovery instrument. The ECA defined traceability as the ability to track money from source to destination, including information on actual costs. It emphasized that citizens should know not only who benefits and what funds are spent on, but also how much is spent. (European Court of Auditors)

The ECA found that RRF funds were traceable and transparent only “to a certain extent” in sampled member states. It reported gaps in the collection and use of information, publication of results, and information on who ultimately benefits from the funds and by how much. It also found that transparency rules did not provide full disclosure on the flow of funds, and that information was insufficient regarding final recipients, actual costs, and results. (European Court of Auditors)

This is highly significant. The EU has advanced institutions, strong legal frameworks, and professional audit systems. Yet even there, when funds move through national budgets, implementing bodies, public procurement, grants, loans, contractors, and final recipients, traceability becomes difficult.

The lesson is not that democracy fails. The lesson is that large public funding systems require engineering-grade traceability.

Why “funds were utilized” is not enough

The phrase “funds were utilized” is often too weak. It tells us money left an account. It does not tell us whether public value was created.

A better accountability sentence would be:

“The funds were released under project code X, received in account Y, spent through contract Z, verified against measurement book A, linked to invoice B, paid to contractor C, and resulted in asset D, which was physically verified and entered into the asset register.”

That is traceability.

In public projects, the ideal audit trail should connect:

Sanction order → budget head → fund release → project code → implementing agency → tender → contract → work order → invoice → measurement book → payment → physical asset → completion certificate → asset register → outcome.

If any link is missing, the project may still exist — but accountability becomes weaker.

Why democracies tolerate weak traceability

There are several reasons.

First, political incentives favor announcements over closure. Politicians gain more visibility from launching schemes than from reconciling cashbooks, closing audit paras, and publishing final-recipient data.

Second, public funds are often fungible. Once money enters the treasury, it can be mixed with tax revenue, borrowing, grants, and other receipts. Fungibility is not always wrong, but it makes source-to-use mapping difficult.

Third, government accounting is often budget-head driven, while public value is project driven. A budget may show expenditure under a department, but citizens want to know which bridge, school, substation, or hospital was created.

Fourth, audit institutions often work after the event. By the time audit findings emerge, political leadership may have changed, officers may have transferred, contractors may have closed claims, and public attention may have moved on.

Fifth, many systems record financial movement but not physical outcome. A payment voucher proves payment. It does not prove quality of work.

The real risk: not only corruption, but non-learning government

The danger of poor traceability is not only theft. It also produces a non-learning state.

If government cannot trace money to outcomes, it cannot know which schemes worked, which contractors performed, which departments delayed execution, which assets failed early, which cost estimates were unrealistic, and which interventions should be stopped.

This is exactly like a manufacturing organization that records production volume but does not track defects, rework, field failures, warranty claims, supplier batches, or root causes. Such a system may appear busy, but it cannot improve.

A government that cannot trace funds cannot learn from expenditure.

What should be done?

Democracies need stronger public-finance interlocks. The following reforms are essential.

Every major government-sponsored project should have a unique project ID from approval to completion. This ID should follow the project through budget, treasury, procurement, contract, invoice, payment, asset register, and audit.

Borrowed funds and large grants should be mapped to declared purposes. If funds are pooled into the treasury, the government should still publish a transparent source-to-use reconciliation.

All contractor payments should be linked to measurement books, milestone certificates, geo-tagged progress, quality records, and asset registers.

Utilisation certificates should not be treated as ceremonial paperwork. They should be digitally linked to underlying invoices, bank payments, work completion, and physical verification.

Public dashboards should not merely show “amount spent.” They should show sanctioned amount, released amount, spent amount, contractor, physical progress, revised cost, completion status, and audit status.

Audit findings should have named accountability, deadlines for closure, and legislative follow-up.

For sovereign borrowing, the discipline should be even higher. If a government borrows in the name of development, citizens should be able to see which development projects were financed, how much each received, and what was completed.

Conclusion: democracy needs auditability

Elections give governments legitimacy. They do not automatically give citizens traceability.

A democracy without traceable public money becomes vulnerable to patronage, waste, opacity, and delayed accountability. The public sees announcements, borrowing, budget speeches, and ribbon cuttings — but not always the chain of custody behind the money.

The Kenya Eurobond case shows how borrowed funds can enter the Exchequer and still fail the test of project-level traceability. India’s pending utilisation certificates show how grants can remain weakly documented. The United States’ improper-payment estimates show that even advanced systems struggle with payment integrity. The United Kingdom’s local audit crisis shows that delayed audit can weaken national accounts. The European Union’s recovery-fund experience shows that even sophisticated frameworks can struggle to disclose final recipients, actual costs, and results.

The lesson is clear:

Public money should be traceable like safety-critical material in engineering.

If steel in a bridge needs certification, public money in a democracy needs a chain of custody.

Because without traceability, citizens are not truly auditing government. They are merely trusting it.

References

European Court of Auditors. Special Report 14/2026: RRF Traceability and Transparency – Gaps Remain Regarding the Traceability and Transparency of RRF Funds. (European Court of Auditors)

Government Accountability Office. Payment Integrity: Agencies’ Estimated Improper Payments Increased to $186 Billion in Fiscal Year 2025. (GAO)

National Audit Office. Spending Watchdog Disclaims Government’s Accounts Again. (National Audit Office (NAO))

Office of the Auditor-General, Kenya. Special Audit Report on the Proceeds and Utilization of Eurobond.

Comptroller and Auditor General of India. Annual Technical Inspection Report on Local Bodies, Maharashtra.

World Bank. Treasury Single Account Rapid Assessment Toolkit. (World Bank)

{kind=link}

{kind=link}

{kind=link}